With the dawn of the new AI era, the game is being reset across multiple industries. We are entering a phase where incumbent SaaS players will either transform rapidly, leveraging their existing distribution and resources, or be replaced by “AI-native” startups that rethink products from the ground up. Either way, territorial lines are being redrawn.

Furthermore, thanks to the novel capabilities and interfaces powered by foundation models, we are finally seeing software penetrate industries and use cases that have historically resisted digital transformation.

There is nothing inherently novel about this observation; this transformation has been unfolding for years. We have been actively investing behind it, backing companies like Lens and IVRy in Japan, and MarqVision and Factory in the US.

However, considering the sheer volume of application-layer AI startups springing up in the US, we have been genuinely surprised by how few there are in Japan. There is so much opportunity here. There should be many more entrepreneurs seizing the moment.

Looking back, the adoption of SaaS in Japan followed a very similar trajectory. When we started investing in 2016, “SaaS” wasn’t even a widely recognized term here. We were fortunate to back SmartHR, Kakehashi, Dinii, and many others during those early, uncertain years.

We hope that this is simply history repeating itself; that just as it took time for Japan to birth startups riding the cloud wave, a Cambrian explosion of AI application layer companies is just around the corner.

With that hope, we want to outline where we see the most promising “white space” opportunities for Japanese founders, and where foreign investors should be directing their attention in Japan.

First, does the application layer even survive?

As foundation models get better and cheaper, do application layer companies even matter, or does the model eat everything above it?

Claiming “SaaS is dead” is catchy. But if you are simultaneously investing in the AI application layer then you must believe that there is room for players above the foundation models, just like there was room for SaaS players above the cloud infrastructure players.

We think it survives, with caveats.

Switching costs will be lower than they were in the SaaS era, as AI will enable massive amounts of data and complex workflows to be ported easily. However, network effects, where a platform becomes more valuable as more people use it, will remain a powerful moat.

Beyond that, startups can build defensibility in the following areas:

- Regulatory & Compliance Needs: Companies want to outsource not just non-core workflows, but the responsibility that comes with them (accounting, legal, compliance, security, insurance).

- Vertical Software: These tools are much harder for generic foundation models to disrupt because they require deep industry-specific expertise, an understanding of niche workflows, and complex legacy integrations.

- Hardware Components & Proprietary Data: Physical touchpoints and access to gated, proprietary data will be incredibly hard to dislodge.

- The Orchestration Layer: Companies want to control their own destinies and avoid being locked into a single foundation model. The orchestration layer that harnesses, routes, and coordinates tasks and costs across multiple models will accrue massive value (this was the thesis behind our investment in Factory). Foundation models alone are expensive, and most frontier usage today is subsidized. When the industry has to actually turn a profit, prices go up, and the value of a layer that controls cost and reduces model dependence goes up with them.

- Specialized Models: startups can capture some of the above with their own models, leveraging vertical specific understanding and proprietary data to have better outcomes (efficacy and efficiency) vs. generic foundation models.

Second, where does a local company win?

This is the question that matters most for Japanese founders, because the honest answer has changed.

In the SaaS era, we backed local players when there was a structural or regulatory reason that gave them a real advantage. SmartHR (Japan’s Rippling) worked because employment law, government APIs, and the insurance system are genuinely different here. Dinii (Japan’s Toast) is built on LINE, the messaging app that is dominant in Japan and almost nowhere else. The moats were local differences.

Two of the old moats are weaker now.

Language and cultural localization no longer protect you. A foreign company can translate and culturally adapt a product across every market instantly. This matters most for product-led companies. If a user can sign up and get value with no salesperson involved, there is little reason they need a local Japanese vendor. Self-serve is the most exposed motion in the country.

Sales-led companies are more insulated, but the clock is faster. This new wave of US AI startups is growing so quickly, and carrying such high valuations, that they are going international far earlier in their lives than the last generation did. They have to, to sustain the growth their investors have priced in. Within Asia, Japan is the obvious first stop. It is large and willing to pay, and unlike most of the region it is open for business. The competition shows up earlier than it used to.

So Japanese founders need to go far beyond cloning something that is working elsewhere, and think about why the local company structurally wins here.

A few answers still hold. Work where someone has to own the regulatory risk. Proprietary local data. Deep wiring into local systems and hardware. Or a vertical narrow enough that no global player will bother to localize it quickly. If none of those apply, you are building a translation layer on top of someone else’s product, and that is a precarious position to be in when a highly capitalized foreign player enters Japan.

LegalOn is the clearest current example. It built its AI contract-review platform on lawyer-supervised Japanese legal content, the kind of proprietary, regulation-bound data a foreign entrant cannot easily copy, and it now reaches over 30% of listed companies.

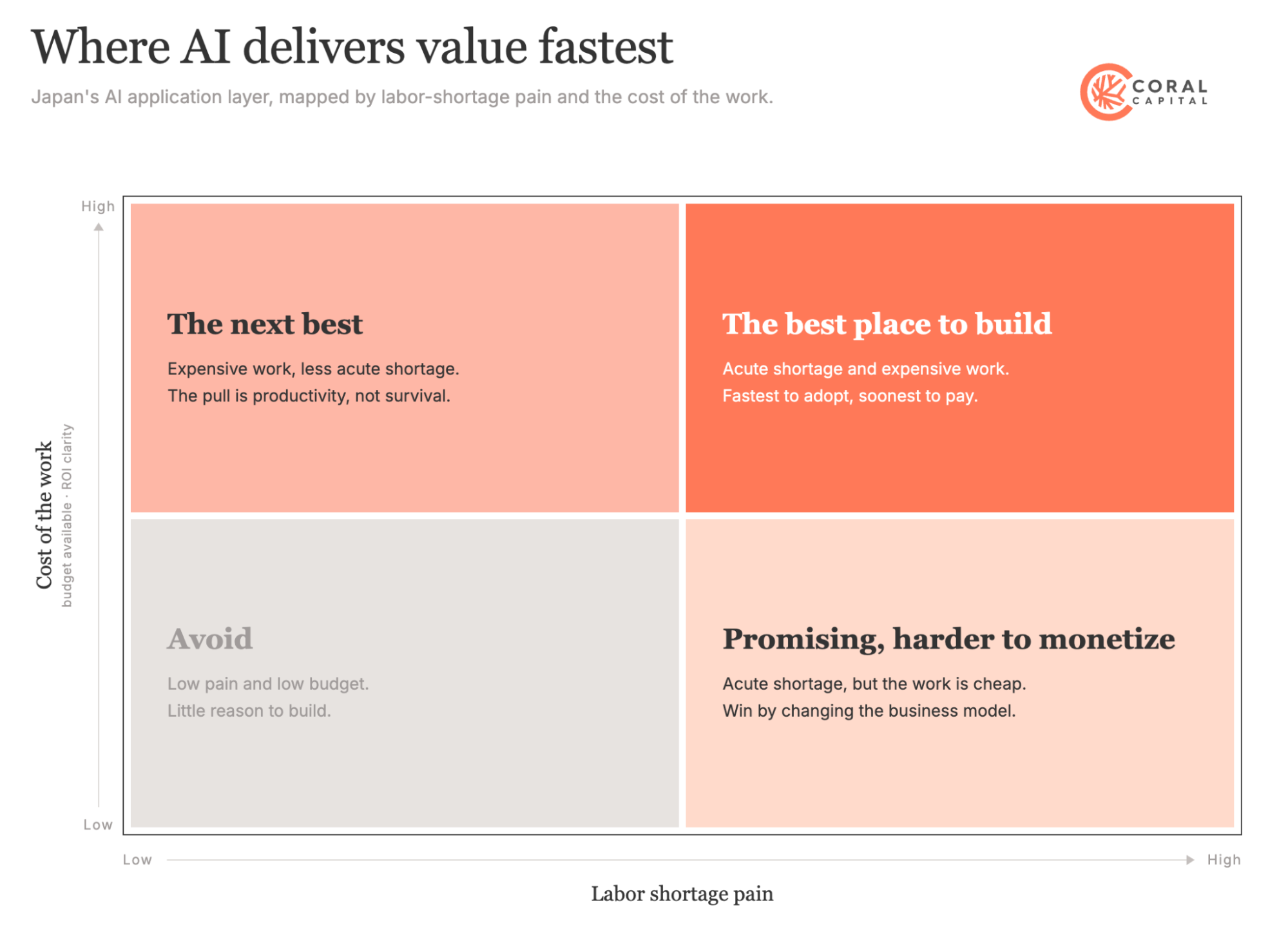

Third, where does AI deliver value fastest?

Once you have a reason to win, the next filter is where the value lands quickly. Map out industries into four quadrants. The x-axis is labor shortage pain. The y-axis is the cost of the work being done, which is a proxy for the budget available and the obviousness of the ROI. The top right, where the pain is acute and the work is expensive, is where AI gets adopted fastest and paid for soonest.

a16z looked at this from another angle: where AI is actually being adopted, not where it is theoretically capable. The work that goes first is text-based and repetitive, kept honest by a human in the loop, and easy to verify once it is done. The work that resists tends to involve the physical world, high-trust relationships, or outputs nobody can check. Keep that filter in mind alongside the quadrants. Note that some of the most acute shortages in Japan, construction trades, truck drivers, hands-on care, are problems for robotics and autonomous vehicles, not for the application software this post is about. But if you can figure out the problems in the physical world as well, the upside will be astronomical.

Japan’s labor shortage is acute. By 2035, Persol and Chuo University project a shortfall equivalent to 3.84 million workers per day, 1.85 times worse than 2023 (Persol). Bankruptcies caused specifically by labor shortage hit a record 441 cases in fiscal 2025, the first year ever above 400 (Teikoku Databank). The pain is everywhere, which is why the x-axis ends up mattering more than the y-axis here.

Top right (high shortage, high-cost work). The best place to build.

- Software and IT. “Information services” is consistently the single most shortage-stricken sector in Japan, with roughly two-thirds of firms reporting they cannot staff it, driven by an acute engineer shortage (TDB). Expensive people, desperate demand, and the work is software itself. This is where the AI coding tools have broken out globally. With that said, there are already many players competing here, both globally and in Japan.

- Clinical documentation and healthcare back-office. Medical and welfare ranks among the worst-hit sectors in Persol’s 2035 projection (Persol). Part of that is a shortage of bodies, which software cannot fix. But a large share of the cost is expensive clinicians losing hours to notes, coding, and intake, and that paperwork is exactly what an AI scribe like Abridge takes off their plate. It is why Abridge spread across US health systems so quickly.

- Accounting, audit, and tax. High-value financial knowledge work sitting on an aging professional base, built from document- and number-heavy workflows that software handles well. This is the kind of expensive, automatable desk work where the ROI is easiest to prove.

Top left (high-cost work, less existential shortage). The next best.

- Legal. Expensive professional time, but Japan does not face a lawyer shortage the way it faces an engineer or clerical shortage. The pull is productivity, not survival. Harvey is the global proof point, and LegalOn is the domestic one.

- Corporate finance and FP&A. High-value analytical work where the constraint is throughput rather than headcount collapse.

- Consulting, strategy, and research functions. Expensive output, people are available, clear automation upside.

Bottom right (high shortage, low-cost work). Also promising, but harder to monetize.

- Clerical and administrative work. Persol ranks clerical staff as the single largest occupational shortfall in the country (Persol), and it is about the most software-replaceable work there is: data entry, scheduling, invoicing, form-filling. The catch is that the labor is cheap, so you are pricing against a low bar. LayerX’s Bakuraku shows how large the prize can still be: by automating back-office finance work end to end across more than 20,000 companies. The company reached ¥10B in ARR by early 2026 (LayerX). Its design goal is the tell, not to make the work easier but to make it unnecessary, with people left to confirm and judge.

- Front-line customer service. Contact centers and inbound phone and inquiry handling run chronic shortages at low wages, and the work sits squarely in what software now does well.

- Restaurants and retail operations. Reservations, inquiries, orders, and listings are all automatable. But restaurant operating margins run around 2%, which leaves almost no room to pay for software. The pain is real and the budget is limited.

Painkillers get paid before vitamins

Another thing to consider is whether your product is a painkiller or a vitamin. Improving efficiency is a vitamin. Solving a problem the customer literally cannot solve today is a painkiller. Painkillers get paid first, and get paid more.

There is a level beyond painkiller worth aiming for. The most valuable vertical AI does work no human team could do at all, usually because of scale. Netic, a US company serving home-services businesses, runs an autonomous revenue engine that answers every call and message the moment it lands, at any hour, and holds up when a heatwave sends demand spiking in a single day. No realistic level of staffing covers that demand the instant it arrives, around the clock.

IVRy, a portfolio company, is another strong example. It automates phone handling, and it did not start in the enterprise but in SMBs: clinics, restaurants, small operators who simply could not answer the phone with the staff they had. The value was not “be more efficient.” It was “this gets handled at all.” It grew from a ¥3,000-a-month product into a service now used across all 47 prefectures and more than 90 industries, having raised over ¥10B.

The throne is yours for the taking

In Japan, where the demographic crisis has made labor shortages an acute, economy-wide reality, the opportunities to build meaningful AI applications are plentiful.

Of course, the Total Addressable Market (TAM) must be large enough to justify venture scale. But for founders who can identify deep vertical pain points, leverage local structural nuances, and build true “painkillers,” the domestic market still feels wide open.

We would love to hear what you are building or thinking about building. Let’s talk.